Smart Tax Planning: Ultimate 5 Tips For Women in FY24

Ever wondered how harnessing the art of smart tax planning could potentially transform your financial landscape? As we step into the fiscal year 2024, discover the five crucial tips that could empower women to wield tax management as a tool for not just savings, but also building a more resilient and prosperous financial tomorrow.

Excerpt:

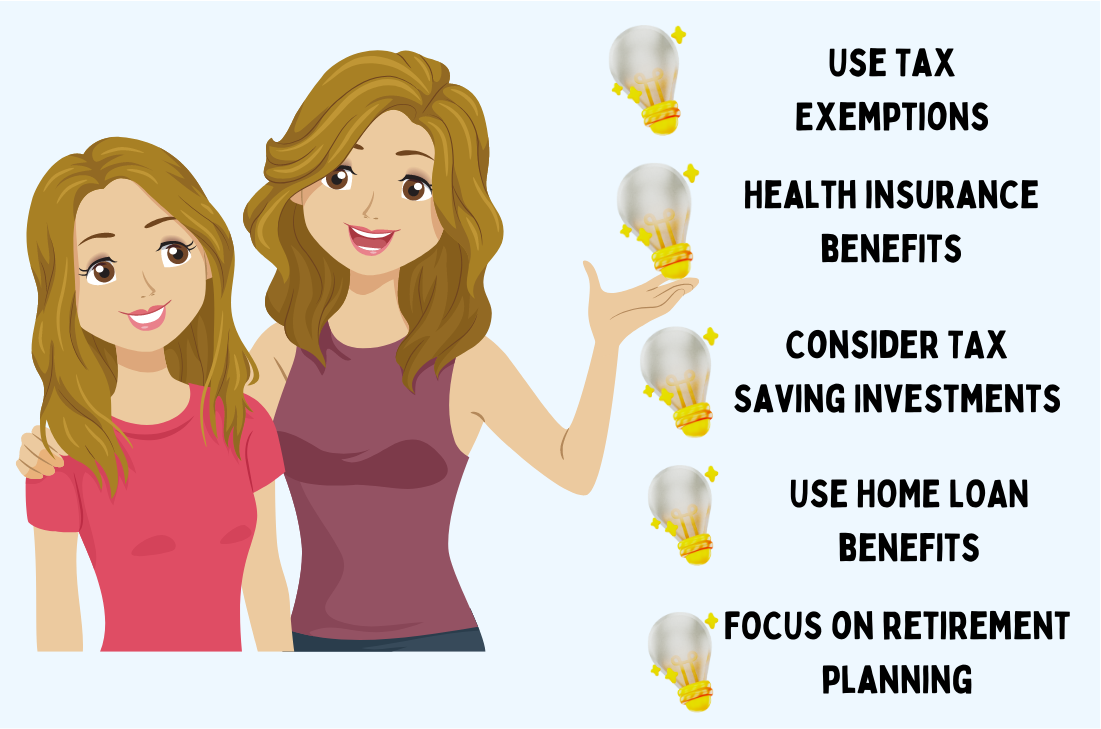

- Use Tax Exemptions

- Health Insurance Benefits

- Consider Tax-Saving Investments

- Use Home Loan Benefits

- Focus on Retirement Planning

1. Use Tax Exemptions: First Step Towards Smart Tax Planning

Women can maximize their tax savings by taking advantage of various exemptions and deductions. They can claim a standard deduction of up to INR 50,000 on their income, reducing their taxable income.

Additionally, under Section 80C, they can invest up to INR 1.5 lakh in tax-saving instruments like Public Provident Fund (PPF), National Savings Certificate (NSC), and Employee Provident Fund (EPF). These investments not only help in tax reduction but also encourage long-term savings.

2. Health Insurance Benefits: Second Step Towards Smart Tax Planning

Women can secure their family’s health and save on taxes simultaneously. Under Section 80D, they can deduct premiums paid towards health insurance policies for themselves, their spouse, children, and parents from their taxable income.

This provision not only promotes preventive healthcare but also provides financial relief in case of medical emergencies.

3. Consider Tax-Saving Investments: Third Step Towards Smart Tax Planning

Women have options to invest strategically for both their financial goals and tax benefits. For instance, the Sukanya Samriddhi Yojana (SSY) is an excellent option for securing their daughter’s future.

By investing until the daughter turns 21, women can ensure a substantial corpus for her education or wedding. Additionally, Equity-Linked Savings Scheme (ELSS) mutual funds offer potential for higher returns while reducing tax liability under Section 80C.

Exploring investment avenues like these helps in growing wealth while staying tax-efficient.

4. Use Home Loan Benefits: Fourth Step Towards Smart Tax Planning

Women who have availed home loans can capitalise on attractive tax benefits. Under Section 80C, they can claim deductions on the principal amount repaid, while Section 24 offers deductions on the interest component.

The Budget of 2016 also introduced an extra deduction of Rs 50,000 on the interest component of their home loan, provided it’s their initial residential property purchase, with specific conditions on the property value and loan amount. These benefits reduce the overall tax burden and encourage women to invest in real estate.

5. Focus on Retirement Planning: Fifth Step Towards Smart Tax Planning

Women should prioritize long-term financial security through effective retirement planning. The National Pension System (NPS) and Employee Provident Fund (EPF) provide not only attractive returns but also offer tax benefits.

Contributions to these schemes qualify for deductions under Section 80CCD(1B) and reduce taxable income. By building a substantial retirement corpus, women can ensure a comfortable and financially stable post-retirement life.

By leveraging tax exemptions, embracing health insurance benefits, exploring tax-saving investments, capitalising on home loan advantages, and focusing on retirement planning, women can not only reduce their tax burdens but also pave the way for a more smart tax planning.

With careful consideration and strategic implementation of these tips, women can chart a course towards financial empowerment and prosperity.