Guaranteed Return Plan: What is it, Tax Benefits, Eligibility

Are you feeling confused with the myriad types of insurance offered by insurance companies? Which type should you go far? Should you go for less risky? What should be your risk appetite? These questions and more might bug you. A good place to soothe your worries is to think about a Guaranteed Return Plan.

What kind of a plan is this? It’s a plan which is less risky and ensures guaranteed returns. Want to know more? Read ahead.

What is Guaranteed Return Plan?

A guaranteed return plan is a financial product that assures investors a specific rate of return on their investment over a set period. Typically offered by insurance companies or financial institutions, these plans provide principal protection, a fixed interest rate, and a predetermined maturity benefit.

While they offer safety and predictability, returns are often lower compared to riskier investments, and there may be penalties for early withdrawals. Investors considering these plans should carefully review terms, understand potential limitations, and align the investment with their financial goals.

Now that you know what a guaranteed insurance plan is, let us take a look at the benefits of a guaranteed return plan.

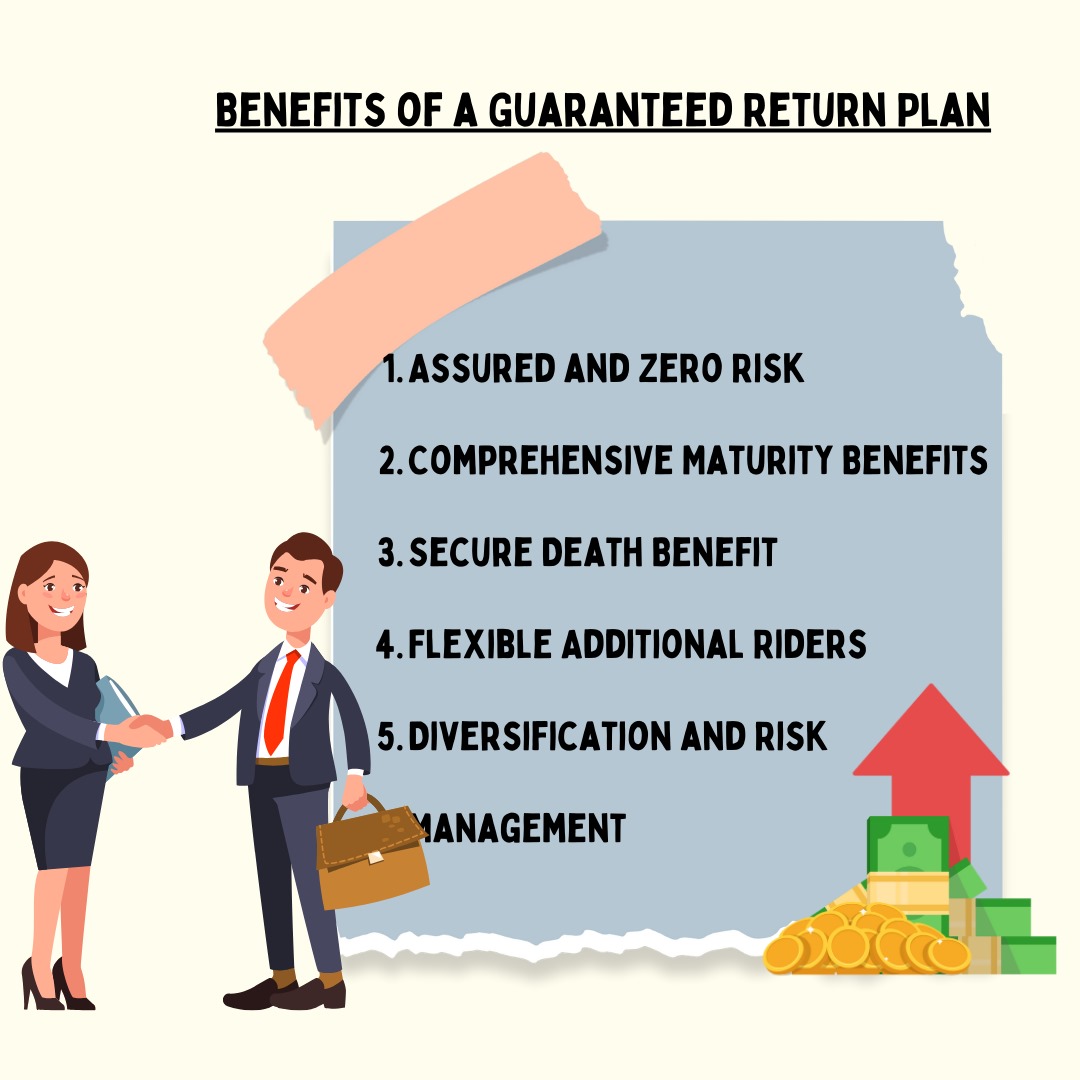

Benefits of a Guaranteed Return Plan

There are several benefits of a guaranteed insurance plan starting from Assured and Zero Risk to Secure Death Benefit. Let’s check each of them here:

- Assured and Zero Risk:

Guaranteed return plans offer a 100% guaranteed return from day one, making them a zero-risk investment. Unlike market-linked options, the returns are not influenced by market fluctuations, providing assurance to policyholders.

- Comprehensive Maturity Benefits:

Policyholders benefit from a guaranteed sum assured, basic reversionary bonus, and, if applicable, a terminal bonus at the end of the policy term. This ensures a comprehensive maturity benefit that aligns with long-term financial goals.

- Secure Death Benefit:

In the unfortunate event of the policyholder’s demise, the nominee receives the death benefit, including reversionary bonuses and terminal bonus, if any. The payouts are distributed over the next 15 years or as specified in the policy, providing financial security to beneficiaries.

- Flexible Additional Riders:

Guaranteed return plans offer optional riders like accidental death benefit, critical illness cover, or waiver of premium benefit. These add-ons enhance coverage, allowing policyholders to tailor their plan based on specific needs, providing additional security and flexibility.

- Diversification and Risk Management:

Including guaranteed return plans in an investment portfolio contributes to diversification and risk mitigation. While maintaining a diversified strategy with various asset classes is essential, adding a guaranteed return plan brings stability, balancing the overall portfolio and offsetting potential risks associated with other investments.

After familiarising yourself with the benefits of a Guaranteed Return Plan, you must check out the tax benefits with Guaranteed Return Plan.

Tax Benefits With Guaranteed Return Plan

From tax deduction to tax exemption, there are several benefits of a Guaranteed Return Plan.

- When you invest in guaranteed return plans, you can deduct up to 1.5 Lakhs from your taxable income under Section 80(C), reducing your overall tax liability.

Tax-Free Returns:

- Returns from guaranteed plans are exempt from income tax under Section 10(10D), ensuring that the money you earn on your investment remains tax-free.

Premium Caution After 5 Lakhs:

- Starting March 31, 2023, guaranteed plans with annual premiums exceeding 5 lakhs will be taxed according to applicable tax slabs, so be mindful of premium amounts to manage taxation effectively.

Now, let’s see if a Guaranteed Return Plan is meant for you.

Who Should Go For Guaranteed Return Plan?

If you fall in one of the following categories, Guaranteed Return Plan is just the right fit for you.

- Cautious People:

If you don’t like taking big risks with your money, Guaranteed Return Plan is the option for you. If you’re the type who wants a steady and surefire return on your investment without worrying about the ups and downs of the market, these plans are a good fit.

It’s like having a financial safety net that won’t surprise you with unexpected losses.

- Retired Folks and Pensioners:

If you’re retired or getting a pension, you probably want a reliable source of income without the stress of market unpredictability.

Guarantee return plans, like fixed deposits or annuities, offer a stable income stream. This is especially helpful when you’re done with the 9-to-5 and want to enjoy your golden years without financial headaches.

- Short-Term Goal Setters

Imagine you’re saving up for a down payment on a house or planning to buy something big soon. Guarantee return plans work well for short-term goals.

You know exactly how much you’ll get back at the end of a set period, helping you meet your targets without worrying about market roller coasters. It’s a straightforward way to make your money work for your short-term plans.

After reading this, if you’ve made up your mind to go for Guaranteed Return Plan, then see below if you’re eligible for it.

Are You Eligible for Guaranteed Return Plan?

The plan is open for individuals aged 18 to 60. Within this age range, you can pick a policy period lasting from 5 to 30 years. This provides flexibility, letting you choose a duration that suits your financial goals and preferences.

With this, you have all the information you need to make a choice on Guaranteed Return Plan. Whether you want to go for this plan depends on your financial planning. Once you’ve done the analysis for yourself, go for it without any ado. And for more such guides, follow NewsCanvass.